Understanding Partnership Taxation: A Guide to Form 1065 and Small Business Taxation | Partnership Tax

By Steven de la Fe, CPA, CFO, Taxfyle on January 16, 2024

In today's evolving business landscape, understanding the intricacies of partnership taxation is essential for entrepreneurs, business partners, and tax professionals. This comprehensive guide delves deep into the realms of partnership tax, taxation processes, and the critical role of Form 1065 in small business taxation. It's a must-read for anyone involved in a business partnership who seeks clarity on tax liabilities, preparation strategies, and effective management of partnership taxation.

What is Partnership Taxation?

Understanding the Basics

Partnership taxation is a system where the IRS taxes the income generated by a business partnership. This system stands in contrast to how corporations are taxed. Rather than being taxed at the entity level, a partnership's income, deductions, gains, and losses are distributed to individual partners. This distribution is based on the partnership agreement or the proportion of ownership each partner has in the business.

| Feature | Description | Impact |

|---|---|---|

| Tax Entity | Partnerships are not considered separate tax entities under federal income tax law. | The partnership itself does not pay income tax. |

| Income Reporting | The partnership files an annual informational return (Form 1065) to report its income, deductions, gains, losses, etc., but it does not pay tax. | Individual partners report their share of the partnership's income or loss on their personal tax returns. |

| Distributive Shares | Each partner's share of the partnership's income, deductions, gains, and losses is called a "distributive share." | Partners report their distributive shares on Schedule K-1, which accompanies Form 1065. |

| Basis | Each partner has a tax basis in their partnership interest. | The basis determines the partner's gain or loss upon sale of their interest and allows for deduction of depreciation on partnership assets. |

| Allocation of Distributive Shares | Partner agreements generally specify how profits and losses will be allocated to each partner. | Different allocation methods can be used, such as profit-sharing ratios, capital accounts, or guaranteed payments. |

| Pass-Through Taxation | Partnership income and losses "pass through" to the individual partners, regardless of whether they are actually distributed. | Partners pay tax on their distributive shares at their individual tax rates. |

| Self-Employment Taxes | Partners are considered self-employed for Social Security and Medicare tax purposes. | Partners are responsible for paying self-employment taxes on their share of the partnership's net earnings. |

| State Taxes | State tax laws on partnerships vary. | Consult with a tax professional about specific state tax implications for your partnership. |

Complexities and Challenges

The 'pass-through' nature of partnership taxation introduces several complexities. Each partner is responsible for reporting their share of the partnership's income on their individual tax returns. This necessitates a thorough understanding of the partnership agreement and the tax implications of shared income and losses. Partners also need to stay abreast of how changes in the partnership, such as new partners joining or existing partners leaving, affect their tax liabilities.

Why is Form 1065 Critical in Partnership Taxation?

Filing Requirements and Importance

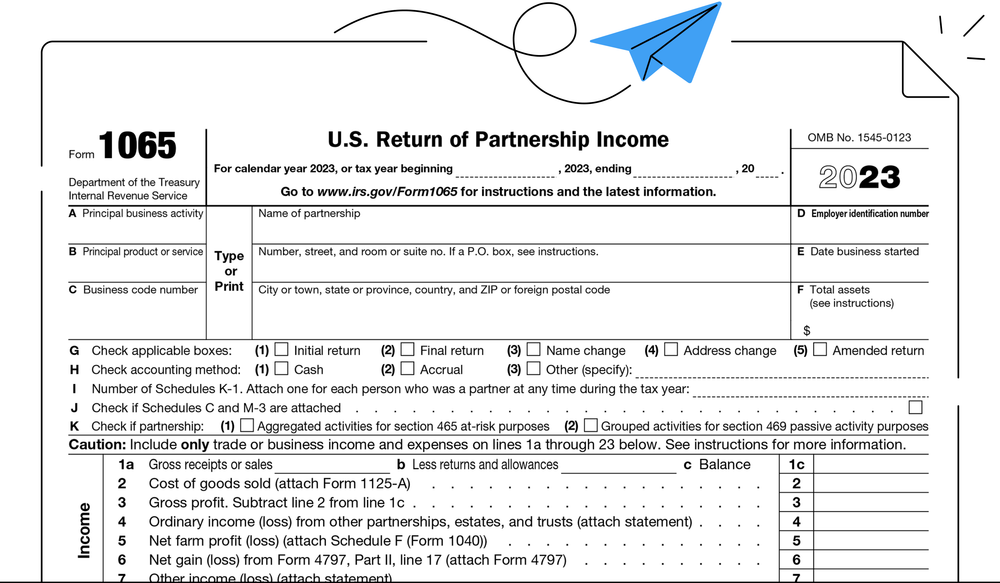

Form 1065, officially known as the Return of Partnership Income, is a mandatory IRS form that all partnerships must file. It serves as a crucial document that details the financial activities of the partnership over the tax year. Through Form 1065, the IRS can assess the partnership's overall financial health and determine the accuracy of the income reported by individual partners on their tax returns.

Detailed Reporting and Compliance

Filing Form 1065 requires a partnership to report its income, deductions, and credits in detail. Compliance with the requirements of Form 1065 is essential for avoiding penalties and ensuring that the partnership and its partners meet their tax obligations. The form also helps partners in preparing their individual tax returns, as it breaks down the distribution of income and losses among them.

How are Partnerships Taxed Differently Than Corporations?

'Pass-Through' Taxation Explained

In partnership taxation, profits and losses pass directly to the partners, who then report these amounts on their individual income tax returns. This system is markedly different from the taxation of corporations, which are taxed independently of their shareholders. Corporations face corporate tax rates, and any dividends distributed to shareholders are taxed again at the individual level.

Implications for Partners

This fundamental difference in taxation has significant implications for tax planning and liabilities for partners. Partners must consider how the partnership's income affects their overall tax situation. This requires an understanding of various tax brackets, applicable deductions, and the potential for self-employment tax on their share of the partnership's income.

Understanding IRS Requirements for Partnership Income Tax

Staying Compliant

Compliance with IRS requirements is a critical aspect of partnership taxation. Partnerships must file Form 1065 annually, report income and expenses accurately, and adhere to specific tax rules and regulations set by the IRS. This compliance is crucial for avoiding penalties and ensuring the partnership's operations are within legal tax boundaries.

Handling Audits and Queries

A solid understanding of IRS requirements also positions a partnership to handle audits and queries from the IRS effectively. This includes maintaining detailed financial records, being transparent about the partnership's financial dealings, and being prepared to justify deductions and credits claimed on tax returns.

The Role of a Small Business LLC in Partnership Taxation

LLCs and Tax Flexibility

Limited Liability Companies (LLCs) enjoy a degree of flexibility in how they are taxed. Many LLCs choose to be taxed as partnerships due to the benefits of pass-through taxation. This choice can be advantageous, particularly for smaller businesses or those looking to avoid the double taxation that corporations face.

Advantages and Considerations

Opting for partnership taxation as an LLC brings certain advantages, such as the distribution of income and losses among members and potential tax savings. However, members of an LLC must be mindful of the tax implications, such as self-employment tax liabilities and the requirement to make estimated tax payments. They must also ensure that their LLC adheres to both federal and state tax regulations, which can vary significantly.

Navigating Estimated Tax Payments for Partnerships

Understanding Estimated Taxes

Partners in a partnership may be required to make estimated tax payments throughout the tax year. This is particularly important if they anticipate owing taxes due to their share of the partnership income. Estimated tax payments are a way to pay tax on income that is not subject to withholding, including income from partnerships.

Calculating and Paying Estimated Taxes

To calculate estimated taxes, partners must estimate their share of the partnership's income for the year and their total tax liability. This includes income tax, self-employment tax, and any other taxes they might owe. Partners should make these payments quarterly to the IRS to avoid underpayment penalties. Effective tax planning throughout the year can help accurately estimate and timely pay these taxes.

Decoding Schedule K-1 and Its Importance in Partnership Taxation

Purpose of Schedule K-1

Schedule K-1 is an IRS form that is a critical part of partnership tax returns. It reports each partner's share of the partnership's income, deductions, and credits. The information on Schedule K-1 is used by partners to fill out their individual tax returns, ensuring that they accurately report their share of the partnership's income and deductions.

Reading and Using Schedule K-1

Partners must carefully review their Schedule K-1 to understand their tax responsibilities. The form provides detailed information about the type of income the partnership receives, such as ordinary, rental, or interest income. It also includes information about deductions and credits that the partner is entitled to claim. Understanding Schedule K-1 is essential for partners to accurately file their tax returns and avoid errors that could lead to IRS audits or penalties.

Tax Deductions and Credits Available to Partnerships

Maximizing Deductions

Partnerships can claim various tax deductions and credits, significantly reducing their taxable income and enhancing overall profitability. Common deductions include business expenses such as rent, utilities, salaries, and equipment purchases. Additionally, partnerships may qualify for specific tax credits related to activities like research and development or environmental improvements.

Navigating Complex Deductions

It's important for partnerships to understand the nuances of tax deductions. Some deductions may have limitations or specific eligibility criteria. For instance, the deduction for business meals is subject to certain conditions, and the amount that can be deducted may vary. Partnerships should also be aware of deductions that are often overlooked, such as deductions for retirement plan contributions or health insurance premiums for self-employed partners.

The Impact of State Tax Laws on Partnership Taxation

State vs. Federal Taxation

While federal tax laws are consistent across the United States, state tax laws can vary widely from one state to another. Partnerships need to be aware of the specific tax laws and regulations in the states where they operate. This includes understanding the state tax rates, filing requirements, and any special state-specific deductions or credits.

Navigating Multi-State Operations

For partnerships operating in multiple states, understanding and complying with each state's tax laws can be challenging. Partnerships must determine their nexus in each state: the level of business activity that subjects them to state taxation. They must also allocate and apportion their income among the states in which they operate, based on each state's tax laws. This requires careful planning and record-keeping to ensure compliance and optimize tax liabilities.

Best Practices for Tax Preparation and Filing in Partnerships

Effective Tax Planning

Effective tax planning is essential for partnerships to manage their tax liabilities and ensure compliance. This includes maintaining accurate and detailed financial records, understanding the tax deadlines, and planning for estimated tax payments. Partnerships should also consider seeking professional tax advice, especially when dealing with complex tax issues or changes in tax laws.

Avoiding Common Pitfalls

Common mistakes in partnership tax preparation include failing to file Form 1065 on time, inaccurately reporting income or deductions, and not properly maintaining financial records. Partnerships should avoid these pitfalls by staying informed about tax regulations, being diligent in record-keeping, and regularly reviewing their tax strategies. Seeking professional tax advice can also help identify potential issues and ensure accurate and compliant tax filing.

Key Takeaways: Navigating How Partnerships Are Taxed | File Form 1065

- Understanding Income Tax in Partnerships: Partners must pay income tax on their share of partnership profits, as reported on their personal income tax return. This is essential under the Uniform Partnership Act, which guides how partnerships are taxed.

- The Role of Deductions: Deductions play a crucial role in reducing the taxable business income of a partnership. These deductions can range from business expenses to contributions towards social security and medicare taxes.

- General and Limited Partnerships: Both general partnerships and limited partnerships must adhere to partnership taxation rules. However, the liability and involvement in management differ, impacting how partnership income or loss is allocated and taxed.

- Business Income and Personal Income Tax: Partnership business income is taxed at the personal income tax level for each partner. Partners must report this income on Form 1040 and pay any taxes owed, including estimated quarterly tax and self-employment tax contributions.

- Importance of a Written Partnership Agreement: A written partnership agreement states the terms for distribution of profits and losses, impacting how partners file taxes and pay income tax. It is also crucial for defining the partnership's tax responsibilities, especially in filing Form 1065 and Schedule K-1.

- Schedule K-1 and Tax Forms: The K-1 form is pivotal in partnership taxation, detailing each partner’s share of profit and loss for tax purposes. Partners use this form alongside other tax forms like IRS Form 1065 and Schedule to file their taxes accurately.

- Social Security Taxes and Medicare: Partners in a partnership must pay taxes on their share of the income, which includes contributions to social security taxes and medicare. This is part of the partnership’s tax obligations under federal income tax laws.

- Small Business Tax Considerations: Small business tax complexities, like business income tax and payroll taxes, must be navigated carefully. Business tax experts can provide guidance on complex tax rules, ensuring compliance and efficient tax management.

- Filing Requirements: Partnerships must file IRS Form 1065 and issue Schedule K-1 to each partner. Partners then use this information to file their personal income tax returns, paying taxes owed on partnership income or claiming losses.

- The Partnership Itself Does Not Pay Taxes: It's key to remember that the partnership itself does not pay federal income tax. Instead, the income or loss is passed through to the partners, who are responsible for reporting and paying taxes on their individual returns.

- Managing Payroll Taxes: If a partnership has employees, it is responsible for managing payroll taxes. This includes withholding the correct amount from employees’ wages and contributing the employer's share of social security taxes and medicare taxes.

- Complex Tax Rules and Compliance: Navigating the complex tax rules of partnership taxation requires diligence and often the assistance of business tax experts. Filing form 1040, understanding the partnership income or loss, and making estimated quarterly tax payments are all part of this process.

- Partnership Files and Tax Records: Maintaining accurate and comprehensive tax records is essential. The partnership files, including IRS Form 1065 and Schedule K-1, should be kept organized and accessible for reference when partners file their tax returns or in case of an IRS audit.

- Self-Employment Tax Contribution: Partners must be aware of their self-employment tax contribution, especially for social security taxes and medicare. This is often a significant part of the taxes owed by partners, particularly in general partnerships where partners actively participate in the business.

How can Taxfyle help?

Finding an accountant to file your taxes is a big decision. Luckily, you don't have to handle the search on your own.

At Taxfyle, we connect individuals and small businesses with licensed, experienced CPAs or EAs in the US. We handle the hard part of finding the right tax professional by matching you with a Pro who has the right experience to meet your unique needs and will handle filing taxes for you.

Get started with Taxfyle today, and see how filing taxes can be simplified.